Automated Debt Collection: Strategies and Platforms for 2026

Debt Collection & Recovery Software

Automated Debt Collection: Strategies and Platforms for 2026

Published on:

May 18, 2026

Managing thousands of accounts across multiple client portfolios quickly turns into operational chaos. Agents follow inconsistent processes, timelines slip, and compliance exposure increases with every manual touchpoint. The booming digital debt collection software market is projected to reach$7+ billion by 2033.

But adopting automation without proper control can introduce new risks rather than solve existing ones. You need systems that standardize execution while maintaining strict oversight across every account.

This is where automated debt collection becomes critical. In this article, we break down how it works, key features to evaluate, proven strategies for agencies, and the top platforms to consider in 2026.

Brief look:

Automation shifts execution from manual to rule-driven systems. Trigger-based actions, workflow progression, and automated queues standardize how accounts are handled across portfolios.

Strategies determine how effectively automation improves recovery. Segmentation, structured workflows, and embedded payment flows ensure automation drives outcomes, not just activity.

Platform choice impacts control and scalability. Tratta, Cogent, and C&R Software each offer distinct approaches across payments, case management, and decisioning layers.

Implementation challenges can offset automation gains if not managed. Data quality issues, workflow misalignment, and over-automation introduce operational and compliance risks.

Long-term success depends on controlled execution and continuous refinement. Agencies must monitor performance, adjust workflows, and rely on systems that maintain visibility and compliance integrity.

What Is Automated Debt Collection in Third-Party Collections

Automated debt collection refers to the use of rule-based systems to manage high-volume recovery workflows across multiple client portfolios. Instead of relying on agent-driven actions for every account, agencies use structured automation to standardize communication, payment handling, and account progression.

The goal is not just speed, but consistency and control across diverse portfolios, each with its own requirements and compliance considerations.

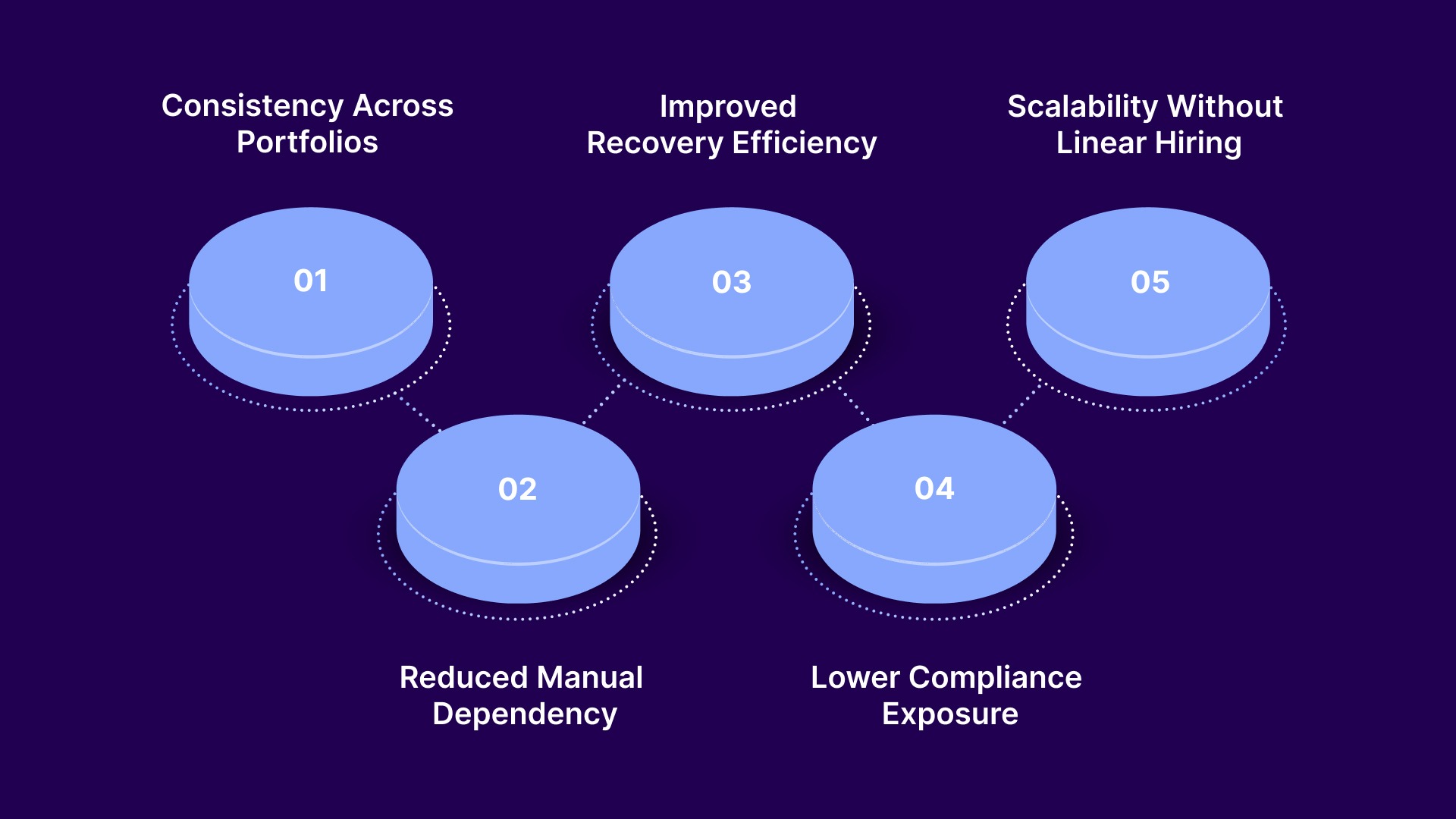

Why it matters for agency operations:

Consistency Across Portfolios: Standardized workflows reduce variation in how accounts are handled, regardless of client or agent.

Reduced Manual Dependency: Automation minimizes reliance on individual agents, lowering the risk of process gaps and delays.

Lower Compliance Exposure: Rule-based systems help enforce consistent adherence to regulatory requirements.

Scalability Without Linear Hiring: Agencies can handle higher volumes without proportionally increasing headcount.

We now move from definition to execution. In the next section, we break down the core features that define automated debt collection systems for agencies.

Key Features of Automated Debt Collection Systems for Agencies

Agencies need to rely on systems that structure workflows, enforce consistency, and maintain compliance across portfolios. These features go beyond basic task automation and focus on controlling how accounts move through the recovery lifecycle.

Core system capabilities agencies rely on:

Workflow Automation: Rule-based workflows move accounts through predefined stages based on triggers and conditions. This reduces manual handling and ensures consistent treatment across all portfolios.

Communication Management: Outreach sequences are scheduled and executed based on account status and predefined rules. This helps maintain consistent contact patterns while reducing agent-driven variability.

Payment Integration: Payment options are embedded directly into collection workflows at key stages. This allows accounts to resolve faster without delays caused by disconnected payment systems.

Compliance Controls: System-level rules enforce communication timing, frequency, and process constraints. This reduces the risk of non-compliant actions across different jurisdictions.

Audit Reporting: Every action taken on an account is logged and traceable within the system. This provides clear visibility for internal reviews and external compliance requirements.

Tratta supports these through structured, rule-driven workflows designed for agency operations. Its system enforces compliance controls at the workflow level, reducing reliance on manual oversight.Schedule a free demo today.

Automation changes how collection work gets executed at a process level. Instead of relying on individual agent decisions, systems apply predefined logic to drive consistency across every account. This shift allows agencies to control execution across portfolios while maintaining visibility into each step.

How automation works in practice across agency workflows:

Trigger-Based Actions: System rules initiate actions based on account events such as placement, inactivity, or partial payments. This ensures accounts move forward without waiting for manual intervention.

Rule-Driven Progression: Accounts advance through collection stages based on predefined conditions and timelines. This removes guesswork and standardizes how cases are handled across portfolios.

Automated Queues: Work is assigned dynamically based on account status, priority, or risk level. This helps agents focus only on where intervention is required instead of managing entire account lifecycles.

Time-Based Execution: Actions such as follow-ups, reminders, and escalations are scheduled automatically. This maintains consistent pacing across accounts without relying on agent tracking.

Continuous Feedback Loops: System data tracks outcomes across workflows and identifies patterns in performance. This allows agencies to refine rules and improve execution over time.

We now move from execution mechanics to strategic implementation. In the next section, we break down practical strategies to attain higher debt recovery by automating debt collection processes for collection agencies.

Strategies to Use Automated Processes for Improving Recovery

Automation delivers results only when applied with clear intent. Agencies need to move beyond enabling features and focus on how those capabilities drive better recovery outcomes across portfolios.

The strategies below show how to use automated systems to improve execution, consistency, and account resolution.

1. Segment Accounts Early

Segmentation ensures that accounts are not treated uniformly, which often leads to missed recovery opportunities. Automated systems allow agencies to group accounts based on balance, age, risk, or client requirements.

To apply segmentation effectively:

Define Segmentation Rules: Group accounts by key variables such as balance size, delinquency stage, or portfolio type.

Assign Workflow Paths: Map each segment to a predefined collection strategy with specific actions and timelines.

Adjust Based on Performance: Refine segments over time using recovery data and account behavior trends.

2. Standardize Workflow Paths

Inconsistent handling across accounts reduces recovery efficiency and creates operational gaps. Automation allows agencies to enforce structured workflows that guide every account through defined stages.

To standardize execution:

Build Stage-Based Workflows: Define clear steps for early, mid, and late-stage collections.

Apply Conditional Logic: Use rules to adjust workflows based on account responses or activity.

Limit Manual Overrides: Restrict deviations to maintain consistency across portfolios.

3. Automate Communication Timing

Delayed or inconsistent outreach often results in lower recovery rates. Automated systems ensure that communication happens at the right time and in the correct sequence.

To improve outreach execution:

Set Communication Schedules: Define when and how often accounts are contacted based on their status.

Align Messaging With Stages: Match communication tone and content to the account’s position in the workflow.

Trigger Follow-Ups Automatically: Ensure no account is missed due to manual delays.

4. Integrate Payment Within Workflows

Recovery improves when payment options are introduced at the right moment. Automation ensures that payment opportunities are embedded directly into the collection process.

Link Payments to Workflow Progression: Move accounts forward automatically after payment activity.

Reduce Friction in Payment Steps: Minimize delays between intent and completion.

5. Use Data to Refine Execution

Automation generates consistent data across accounts, which can be used to improve recovery strategies. Agencies that actively use thesedashboards can optimize workflows and increase effectiveness over time.

To continuously improve performance:

Track Workflow Outcomes: Monitor how accounts perform at each stage.

Identify Drop-Off Points: Analyze where accounts stall or disengage.

Update Rules Based on Insights: Refine automation logic to improve recovery rates.

We now shift from strategy to evaluation. In the next section, we review the best third-party debt collection platforms and how they support these automation approaches.

Top 3 Third-Party Automated Debt Collection Platforms for 2026

Selecting a platform requires understanding how each system approaches automation within agency workflows. Some focus on payment-driven resolution, others on case management depth or decisioning layers.

Thesoftware below reflects distinct approaches to automation in third-party collection environments.

1. Tratta

Tratta is a debt collection platform designed to support agency workflows through structured automation and embedded payment capabilities. It enables consumers to resolve accounts through digital channels while maintaining system-level control for agencies.

The platform focuses on reducing manual handling by aligning payment activity with account progression. Its approach centers on maintaining visibility and control across high-volume portfolios.

Key automation features:

Self-Service Resolution: Consumers can access accounts, select payment options, and complete transactions without agent involvement. This reduces workload and accelerates resolution timelines.

Rule-Based Workflows: Account actions are triggered based on predefined conditions such as account status or payment activity. This ensures consistent handling across portfolios.

Embedded Payments: Payment processing is integrated directly into the workflow, allowing accounts to progress without external system dependencies.

Audit Visibility: All actions are logged within the system, providing traceability and supporting compliance oversight.

Agencies need automation that enforces control, not just execution. Tratta structures workflows with built-in guardrails, helping you scale operations without introducing compliance or visibility gaps.Contact us to learn more.

2. Cogent

Cogent is a collections and litigation management platform built for agencies handling complex recovery processes. It is commonly used in environments where accounts require structured case handling across multiple stages, including legal escalation. The platform supports detailed account management with configurable workflows tailored to different recovery paths. Its strength lies in managing complexity rather than simplifying execution.

Key automation features:

Case Workflow Management: Accounts move through structured workflows that support both collections and litigation processes. This ensures continuity across different recovery stages.

Rules Engine: System rules automate task assignment, account handling, and decision flows based on predefined conditions. This reduces manual routing and improves consistency.

Payment Tracking: Payments are recorded and applied within the system, updating account status as actions occur. This keeps workflows aligned with financial activity.

Operational Reporting: The platform provides visibility into account activity and workflow performance for ongoing monitoring.

3. C&R Software (Debt Manager)

C&R Software provides enterprise-level debt collection software through its Debt Manager platform, with a strong focus on analytics and decisioning. The platform combines automation with strategy layers that guide account treatment. Its strength lies in using data to influence how workflows are applied rather than just executing them.

Key automation features:

Decisioning Tools: Data-driven logic is used to determine how accounts are segmented and treated within workflows. This allows for more targeted recovery strategies.

Automated Task Handling: Routine actions such as task assignment and account progression are managed by the system. This reduces dependency on manual coordination.

Analytics and Insights: Performance data is captured and analyzed to refine collection strategies over time. This supports continuous improvement.

Workflow Configuration: Agencies can define how accounts move through different stages based on internal policies and portfolio requirements.

In the next section, we examine the key challenges agencies face when implementing automated debt collection systems and where gaps typically emerge.

Challenges in Automated Debt Collection for Third-Party Agencies

Automation can improve execution, but implementation introduces its own set of risks if not structured correctly. Agencies often face challenges both during rollout and after systems go live, especially when managing multiple portfolios with varying requirements.

Table showing common challenges:

Challenge Area

Where It Occurs

Impact on Agency Operations

Workflow Misalignment

During implementation

Poorly defined rules lead to inconsistent account handling across portfolios.

Data Inconsistency

During implementation

Incomplete or inaccurate data disrupts automation logic and workflow accuracy.

Over-Automation

After implementation

Excessive reliance on automation reduces necessary human oversight and control.

Compliance Gaps

During and after implementation

Incorrect rule configuration can result in non-compliant communication or actions.

Integration Issues

During implementation

Disconnected systems create delays in payments, updates, and account progression.

Limited Visibility

After implementation

Lack of clear reporting makes it difficult to track performance and audit actions.

Rigid Workflows

After implementation

Inflexible systems prevent agencies from adapting to portfolio-specific requirements.

We now move from identifying operational risks to establishing structured controls that mitigate them. In the next section, we outline best practices for implementing automated debt collection within agency environments while maintaining compliance and execution integrity.

Best Practices for Implementing Automated Debt Collection by Agencies

Effective automation depends on how well workflows are structured, controlled, and continuously evaluated. Agencies must align automation with operational realities, regulatory expectations, and portfolio variability to ensure long-term performance.

Best practices include:

Define Workflow Logic Early: Establish clear rules for how accounts move across stages before implementation begins. This prevents inconsistent execution and reduces the need for reactive adjustments later.

Standardize Across Portfolios: Create baseline workflows that apply across client portfolios while allowing controlled variations where required. This ensures consistency without compromising client-specific requirements.

Embed Compliance Controls: Integrate regulatory constraints directly into workflow rules, including timing, frequency, and permissible actions. This reduces reliance on agent judgment and minimizes exposure to compliance risk.

Validate Data Inputs: Ensure that account data is accurate, complete, and consistently formatted before feeding it into automated systems. Poor data quality can disrupt workflows and lead to incorrect account handling.

Continuously Monitor and Refine: Track workflow performance and identify areas where accounts stall or underperform. Use these insights to adjust rules and improve recovery outcomes over time.

Sustained performance depends on aligning these practices with technology that enforces structure and consistency across workflows. Selecting the right platform determines whether automation strengthens operations or introduces new risks.

Conclusion

Without structured automation, agency operations become difficult to control at scale. Inconsistent workflows, delayed outreach, and fragmented systems increase compliance exposure and reduce recovery efficiency across portfolios. As account volumes grow, manual processes create variability that directly impacts performance and audit readiness.

Tratta addresses these challenges by structuring workflows with built-in controls and aligning payments with account progression. Its system-level guardrails reduce reliance on manual oversight while maintaining visibility across every action. This allows agencies to scale operations without introducing compliance gaps or execution inconsistencies.

Adopt automation that enforces control, not just speed. Choose systems that align workflow execution with compliance requirements at every step.Schedule a free demo today.

Frequently Asked Questions

1. How long does it take to implement automated debt collection in an agency?

Implementation timelines vary based on system complexity, integrations, and data readiness. Most agency deployments take a few weeks to a few months, depending on how workflows and compliance rules are configured.

2. Can automated debt collection systems handle multi-state regulatory requirements?

Yes, but only if compliance rules are properly configured within the system. Agencies must ensure that workflows account for jurisdiction-specific communication limits, disclosures, and timing requirements.

3. How does automated debt collection affect agent roles within agencies?

Automation reduces repetitive manual tasks and shifts agents toward exception handling and high-value interactions. This allows teams to focus on accounts that require judgment rather than routine processing.

4. What type of data is required to run automated debt collection workflows effectively?

Agencies need accurate account data, including balances, contact details, account status, and client-specific rules. Incomplete or inconsistent data can disrupt workflows and reduce automation effectiveness.

5. How do agencies measure the success of automated debt collection systems?

Performance is typically evaluated using metrics such as recovery rates, resolution timelines, contact success rates, and compliance adherence. Continuous monitoring helps identify areas for workflow optimization.

Note: This information is not legal advice. Tratta recommends that you consult with your legal counsel to make sure that you comply with applicable laws in connection with your collection and outreach activities.

Sign up for our monthly newsletter

Debt collection insights that keep you compliant and competitive.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.